Heywood

From April 2026, the FCA's targeted support framework changes how organisations help members and consumers make pension and investment decisions. It also sets a clearer expectation: that organisations can show their communications actually helped people understand their options.

Targeted support applies to DC pensions and retail investments. But the standard it sets matters for any organisation explaining complex financial information.

What is targeted support?

Targeted support is a new FCA framework that lets authorised firms provide ready-made investment and pension suggestions to groups of customers in similar financial situations. Unlike full regulated advice, it does not require a detailed assessment of each person's circumstances. Instead, firms design suggestions for defined consumer segments based on shared characteristics such as age, account type, or the decision they are facing.

The aim is to close the advice gap. The FCA estimates around 23 million people in the UK are currently underserved by financial advice and guidance. Targeted support makes help more affordable, accessible and scalable.

Firms that want to offer targeted support must apply for a new regulated activity permission. The authorisation gateway opened in March 2026, and the regime takes effect from 6 April 2026. Unlike regulated advice, targeted support can be offered free of charge, which is central to its reach.

Who does targeted support apply to?

This is where precision matters.

Targeted support applies to DC pensions and retail investments. It covers pension and investment firms, fund managers, platforms, SIPP operators, banks, building societies and financial advice firms. Trust-based pension schemes are also in scope where they relate to DC arrangements.

DB pension schemes, mortgages and non-investment insurance products are not covered. Pensions consolidation and specific annuity suggestions are also excluded.

So if you work in DB pensions or mortgage lending, targeted support is not your regulatory obligation. But the communication standard it introduces and the evidence it expects, has implications well beyond the organisations it directly regulates.

Why this matters beyond DC pensions and investments

Targeted support formalises something that has been building for years: the expectation that organisations prove people understood what they were told, not just that they sent it.

The FCA requires that consumers receiving targeted support end up in a "better position" than without it. That is not a test of whether a message was sent or opened. It is a test of whether it helped someone make an informed decision.

This mirrors Consumer Duty, which already requires FCA-regulated firms to design communications that support understanding, not just meet a disclosure obligation. It also aligns with TPR's growing focus on member outcomes.

The direction of travel is consistent. Across pensions, investments, banking and insurance, the question is shifting: not "did you tell them?" but "did they understand?"

That applies whether you are a DC provider designing a targeted support journey, a DB scheme communicating a buy-out, or a building society explaining mortgage maturity options.

How the FCA's targeted support framework raises the standard

For firms directly subject to targeted support, the challenge is specific and immediate.

They must explain a ready-made suggestion clearly enough that a consumer understands why it applies to them, what it involves and what its limitations are. They also need evidence that the communication worked, because the "better position" test requires outcomes, not assumptions.

A letter or email explaining a product recommendation may not be enough. If an organisation cannot show that customers engaged with and understood the suggestion, it becomes harder to prove targeted support delivered.

This is a practical problem. The FCA expects firms to review and monitor outcomes regularly. Those that can track engagement depth, completion rates and behavioural signals such as follow-up actions or fewer queries will be better placed to meet those expectations.

What this means for organisations outside the framework

For pension schemes, building societies and other financial services organisations not directly subject to targeted support, the relevance is in the standard it sets.

Think about what pension schemes already communicate. Annual benefit statements that need members to understand projected retirement income. Scheme events like GMP equalisation, McCloud remedy, or buyouts that require informed choices within a set window. Transfer value illustrations that ask members to weigh trade-offs between guaranteed and flexible benefits.

Each shares the same challenge as targeted support: explaining something complex and personal to someone who may have limited financial knowledge, in a way that helps them decide.

Building societies face the same issue. Mortgage maturity communications must explain options clearly enough that customers understand each path. Product switch journeys need customers to compare terms and make active choices rather than defaulting into arrangements that may not suit them.

The standard is the same everywhere. Clear, personalised communication that supports understanding, not just information that was technically sent.

How personalised video supports this

Video Engage explains complex financial information through personalised video that adapts to each person's circumstances. Rather than a generic document covering every scenario, it delivers a guided explanation built around the recipient's own data: their figures, their options and language designed to be understood without specialist knowledge.

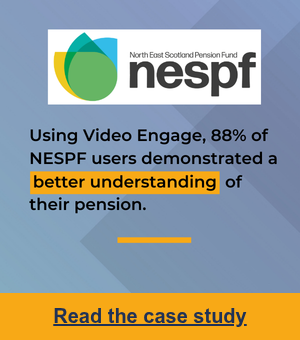

The results are measurable. Working with the North East Scotland Pension Fund, 88% of members reported better understanding of their pension after receiving personalised video communications. Engagement rates for active annual benefit statements rose by 80%. Schemes also report fewer follow-up queries, with the remaining enquiries more focused and action oriented.

These are operational outcomes, not innovation claims. They address the same challenge targeted support is designed to solve: helping people understand financial information well enough to act on it.

Video Engage also generates the engagement data organisations increasingly need. Completion rates, replay behaviour, interaction points and follow-through actions provide clear evidence that a communication was not just received but actively engaged with. For firms subject to targeted support, this supports the "better position" evidence requirement. For others, it offers the same insight into whether communications are doing their job.

The broader direction

Targeted support is one framework, applied to one area of the market. But it reflects a direction that is unlikely to reverse.

Behind every regulatory framework, every compliance obligation and every communication strategy, there is a person trying to make decisions about their financial future. A member weighing up whether to transfer. A customer deciding what to do when their mortgage rate ends. Someone approaching retirement who needs to understand options they have never faced before.

The organisations that consistently meet regulatory expectations tend to start from that point. Not "what does this regulation require us to send?" but "what does this person need to understand?" When the focus is on genuine outcomes, the compliance follows. When it works the other way round, organisations find themselves chasing the next framework.

Targeted support, Consumer Duty, TPR's member outcomes focus: they all point the same way. Clearer communication cuts operational cost, improves outcomes and builds trust. The regulation is catching up with what good practice has looked like for a while.

Whether you are preparing for targeted support, managing complex scheme events, or looking to reduce avoidable queries from unclear communications, the question is the same: when you communicate with customers or members, can you show it worked?